Public equity: investment tactics for the rest of the Year 2021

Hyper-growth might disappoint you this year, so look for monopolies and those that might enjoy strong demand amid constrained supply.

People often ask me what is my investment strategy and how I am adjusting my portfolio given rapid development of the pandemic and economic situation. Year 2020 was very volatile, but overall phenomenal for stock equities. Current year started quite strong for equity markets (returns YTD)👇 :

🇺🇸 Russell2000 +15.5%

🇺🇸 SP500 +11.6%

🇩🇪 DAX +10.6%

🌏 MSCI World +9.7%

🇺🇸 Nasadaq +7.8%

🇵🇱 WIG +6.6%

🇯🇵 Nikkei +5.7%

I believe diversification is a good way to limit volatility of your portfolio and especially effective if you diversify among different types of investment as well as among geographies.

My personal public equity portfolio consist of 3 sub-portfolios, among them:

High (or hyper) growth stocks

Compounders

Cyclicals.

Looking through the lens of my own portfolio I am sharing with you three major tactics for the rest of 2021. I hope you might find it useful.

Tactic no.1 - Limiting exposure to hyper-growth stocks

Definition

Basically, we might distinguish between 3 types of revenue growth for established businesses (>$500m Revenue):

Hyper growth (CAGR over 40%)

Rapid growth (CAGR 20-40%)

Normal growth (CAGR below 20%).

When dividing between categories it is wise to look at 3 or 5-years CAGR instead of 1-year change to have a better understanding of the growth profile.

Growth vs. Value

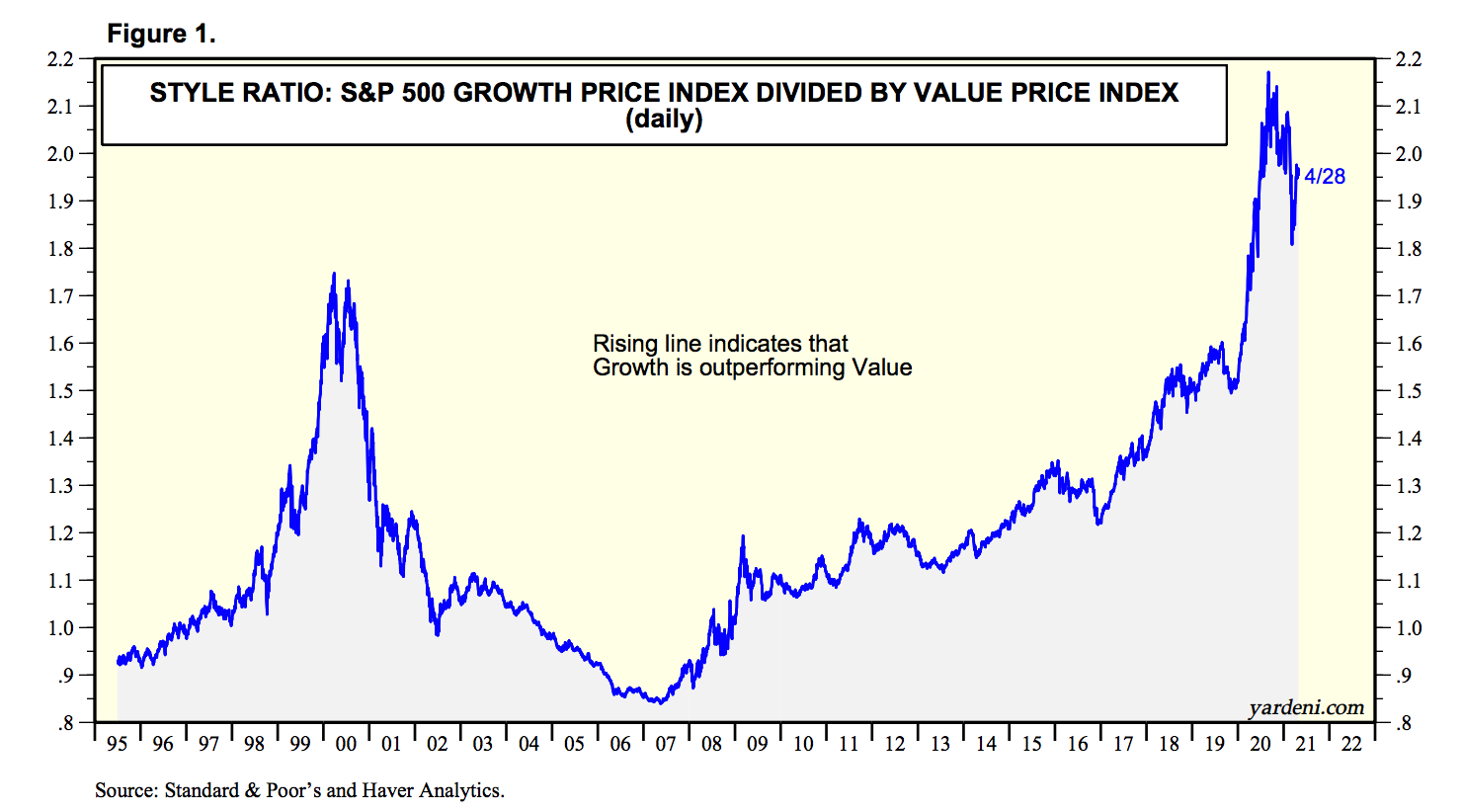

Growth has been a phenomenal investment strategy for the last 13 years, outperforming value strategy by magnitude of 2x - take a look at the chart from Yardeni 👇 (full research here: Style Guide: S&P500 Growth vs. Value):

Inflation risk

Growth has also been super effective since the start of Covid-19 pandemic as bond yields accelerated its path toward 0% yield. However… things are changing rapidly and inflation risk is something you have to take seriously into account (read FT: Investors shore up defences against rapid rises in US inflation):

All over the world demand for goods and components to produce them exceeds constrained supply. I have no idea if that inflation pressure will only be transitory and it will recede next year. What I know for sure however is that you should be discounting your future earnings with higher interest rates (vs. whatever you used in Year 2020) and stress test your portfolio under scenarios that it might go significantly higher. In fact implied probability of CPI (Consumer Price Index) being higher than 3% in the next 5 years is already ~30%.

According to economist Mohamed A. El-Erian:

The Fed should seriously consider following the Bank of Canada’s example by initiating a gradual and careful retreat. The longer it takes to do so, the harder it will be to pull off an eventual normalization without risking both significant market volatility and damaging what should and must be a durable and inclusive economic recovery.

- from Bloomberg’s article: Fed Should Start Tapering, But It Won’t

Why interest rates are so important for (hyper) growth stocks?

Basically, we can divide value of each company into two components:

Present Value of Assets in Place, and

Present Value of Growth Opportunity (PVGP).

VALUE = PV of Assets in Place + PVGO

or

VALUE = (Earnings Y+1 / Cost of capital) + PVGOAs a consequence most hyper growth stocks:

have no earnings or positive cash flows at current state

have its value deep into the future (Growth Opportunity)

have 90% to 100% of company value associated with its Terminal Value (beyond the projected horizon in financial models)

were already valued close to perfection with the lowest interest rates you could imagine.

As high growth stocks are highly dependent on discount factors, in the environment where cash today is worth more then cash tomorrow (inflationary environment) those kind of companies might be under downward pressure.

Take a look at following example:

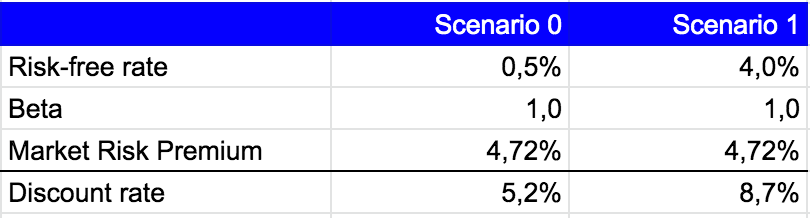

Lets assume we are able to spot a future star - a company to be worth $100 Billion 10 years from now

The question is what is the value of $100 Billion company if risk free rate changes from 0.5% (the bottom of 10Y US bond yields in 2020) to let’s say 4%.

Assuming that: Beta = 1 and Market Risk Premium = 4.72% (from A.Damodaran NYU Stern webpage), the Discount rate is equal to👇:

So what’s the value of that “$100B company” today under each scenario?

That 3.5% differential in Risk-free rate (we’re not yet there, but it’s probable now) or would mean that your future "$100B company is worth 28% less under Scenario 1 vs. Scenario 0. That’s a huge negative change and it’s all due to potential interest rates differential as company stays in our assumption the same, intact. In long term (5-10 years) our total returns would be mainly driven by earnings power. However in short term (1-2 years investment horizon) changes in discount rates might significantly vary your returns.

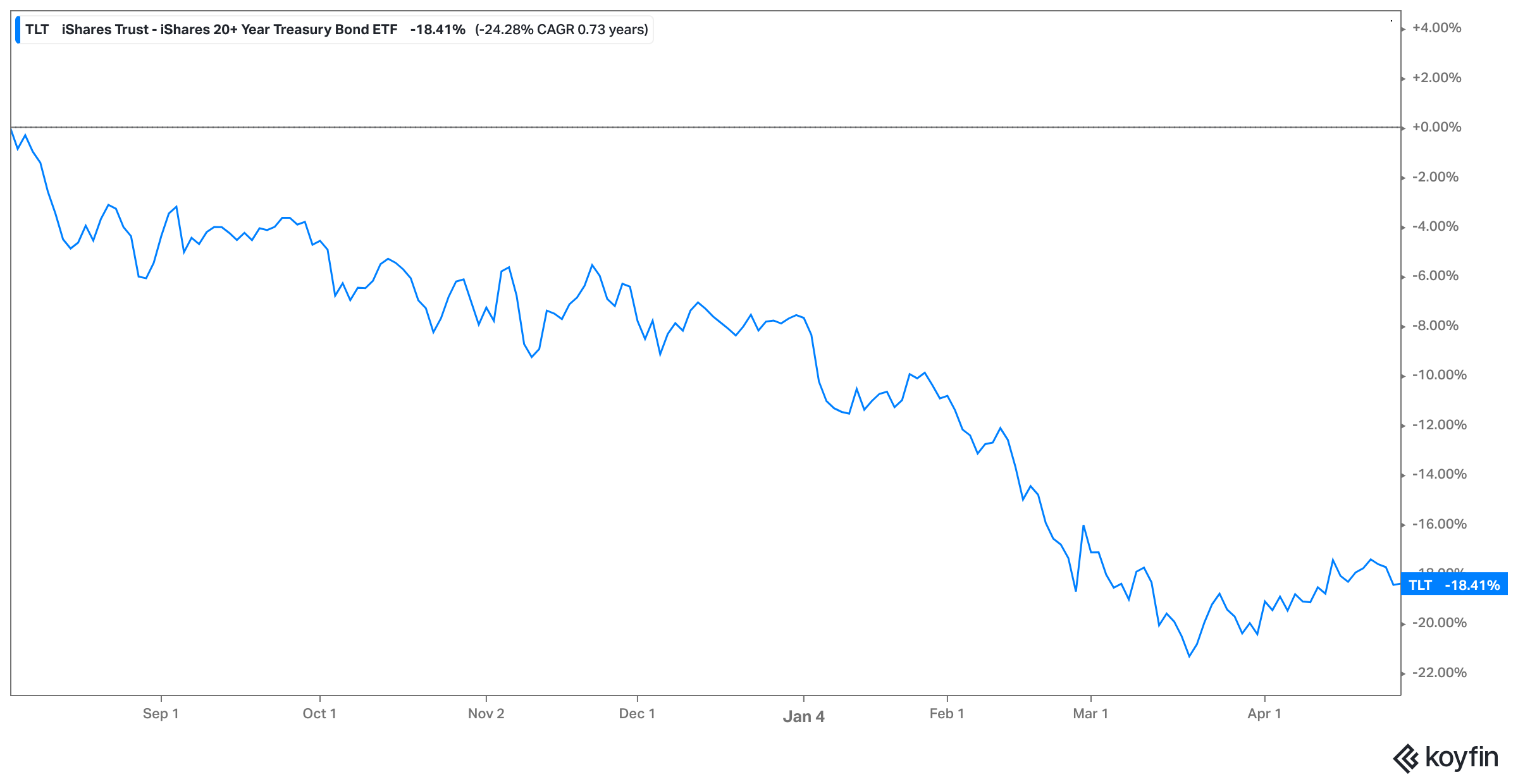

Similarities to bonds

In that regard high growth stocks are similar to long-term bonds (their value is so deep into the future). If someone told you that Bonds are safe, look at chart below:

TLT - ETF representing 20+ Years US Treasury Bonds is -18.4% from the top in Q3’2020!

It is all about discount rates. If you do not want to be highly exposed to the inflation risk, you might consider limiting your exposure at the long end of the curve. Hold only your highest conviction positions!

Tactic no.2 - Investing in Compounders

Compounders take the biggest share in my portfolio. Those are companies I am most comfortable to be invested in for long-term (>5 years investment horizon), regardless of market volatility.

What are the key features of “Compounders”?:

high quality business model

recurring revenue (at least partly)

building dominant and durable intangible assets (i.e. brand recognition)

pricing power over long period of time

able to scale with relatively low-capital intensity

able to grow significantly (15-30% annually, but as they’re established companies, they rarely grow faster).

When evaluating that kind of ‘animal’ you should pay special attention to franchise quality, durability of its business model, industry positioning and management quality.

What are the sources of durability?

Generally, companies build best sustainable competitive advantage and moat by creating intangible assets, which competitors are not able to copy or re-create. Among them are:

brand recognition

customer loyalty

distribution network

intellectual property (IP) / innovation

strong culture.

Overall, compounders are better quality businesses and their superior business model should be reflected in financial strength. They usually enjoy sustainable high return on invested capital (ROIC), which is the result of recurring revenues, superior margins and low-capital intensity. Unlike many smaller hyper-growth businesses they have already proven business model and dominant position in the market.

What I like most about Compounders is the fact that they are more immune to economic shocks given their pricing power and overall superior cash flows. Usually, in downturn economic conditions they are able to increase their market share and often buy competitors through smart acquisitions.

Over time they build monopolistic or oligopolistic position in the market. They are able to innovate and create optionality to grow further.

How value is created?

I believe it is important to invest in companies with high quality management, those who demonstrated their discipline in capital allocation.

BTW: there is a great research on the subject - Capital Allocation – Updated Evidence, Analytical Methods, and Assessment Guidance by Michael J. Mauboussin (Twitter: @mjmauboussin).

Long-term value creation is a function of two components working together:

Revenue growth

Return on invested capital (ROIC).

It is not intuitive for most managers, but company might experience Revenue Growth of three types:

Good growth = value creating; when ROIC > Cost of capital

Meaningless growth; when ROIC = Cost of capital

Value-destroying growth; when ROIC < Cost of capital

Below the Exhibit 👇 from the best introductory book to company valuations: Valuation: Measuring and Managing the Value of Companies

Value increases with all improvements in ROIC, but no all growth creates value. That’s why capital allocation is so important.

In general, Value is very sensitive to growth rate as there is a wide spread between ROIC and Cost of Capital.

What growth strategy creates most value?

McKinsey research shows that organic new product development frequently have the highest value added for each incremental dollar of revenue. That seems to be the reason why Amazon doesn’t sell only books anymore, or why Apple expanded beyond personal computers.

When to buy Compounders?

It’s not easy, as they are so good they are not cheap. Never. 🤷♂️

Take a look at Amazon ($AMZN) 👇 Its P/E ratio with Earnings expected in following 12 months ranged between 60x and nearly 300x for the last 10 years. Unusually high given market P/E ratio in range of ~15 to 25x Earnings for most of the time. In the same time horizon stocks of Amazon delivered +1670% return!

So, you have to focus on long term and their increasing market power. In case of Amazon it has been gradually building its Cash Flow potential.

You also should buy Compounders gradually! Obviously, the best time to buy them is during market corrections. On average, since since 1920, the S&P 500 Index has recorded👇:

5% pullback three times a year;

10% correction once every 16 months;

20% plunge every seven years.

You might also just spread your purchases over longer period of time.

Base rates

Here a small caveat - it’s not that easy to correctly pick Compounders - actually there are very few companies at scale that are able to consistently grow at a rate of >15%. If you would like to understand how rare it used to be study The Base Rate Book by Michael J. Mauboussin.

However, spotting established company that might be able to grow at CAGR of 15%+ for the next 5-10 years, might be much much easier than spotting a future star (hyper-growth company) with valuation justified only under assumption that the company will grow at CAGR of at least 30-40% in a foreseeable future.

I believe that approach should help to generate superior risk-adjusted returns, especially given increased inflation uncertainty.

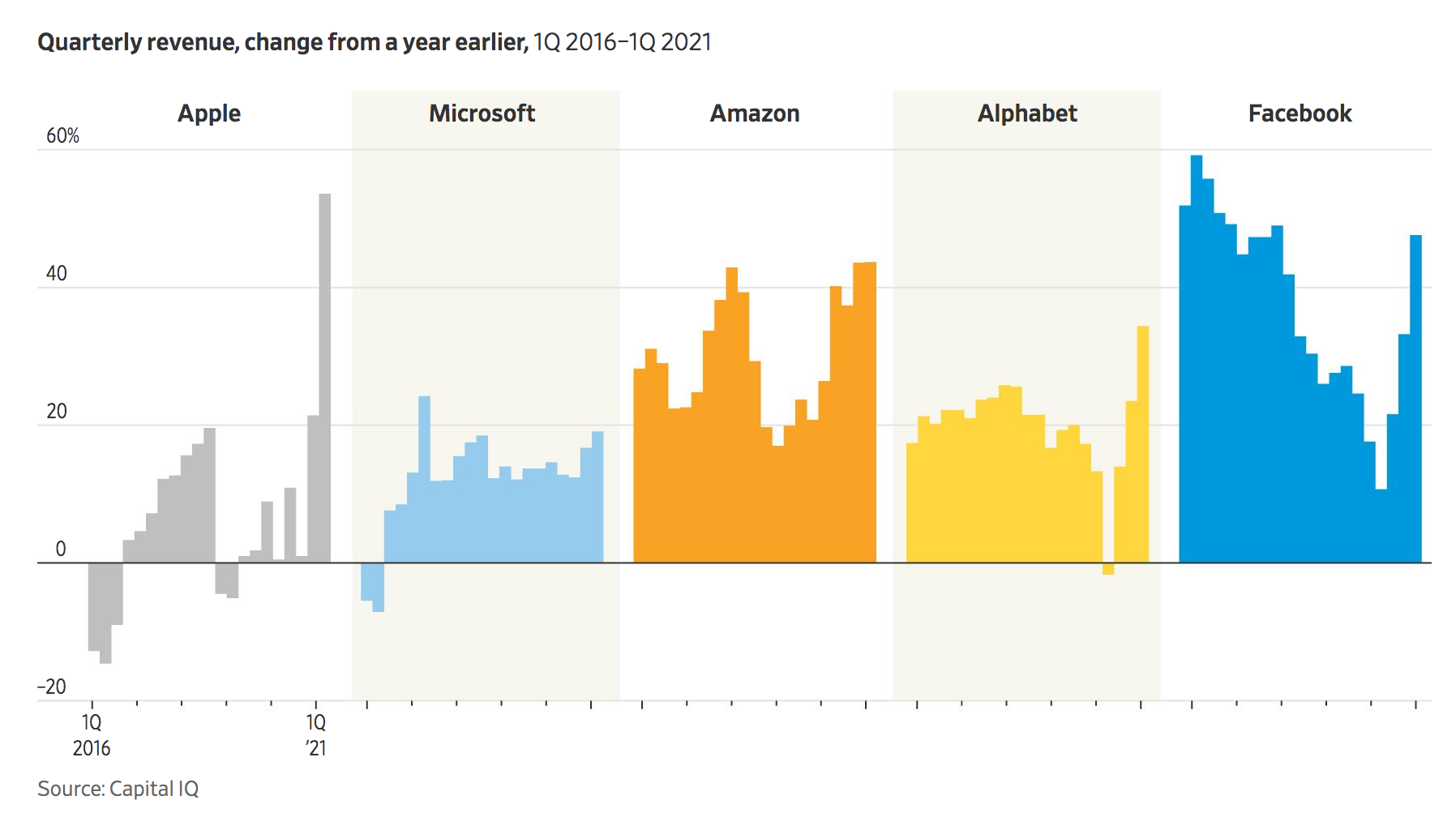

I will not name my picks as there are many quasi-monopolies / oligopolies. Historically, among US stocks FAAMG filled well Compounders’ category. Last week, they published their Q1’2021 earnings reports - all of them did very well, rebounded revenue growth and generated billions of dollars of profits (you can read full WSJ article: Five Tech Giants Just Keep Growing):

Conclusion: Monopolies are a good place to be as an investor. Look for them and hold tight! While they might not be able to deliver 10x return in near future, it’s hard to look for better risk-adjusted returns.

Tactic no.3 - Investing in businesses that might enjoy constrained supply side

In current state of economy with many world imbalances it might actually be wise to look for situations where:

there is a strong demand for goods or services

supply side is inelastic

supply side is working close to full capacity.

When do businesses enjoy constraints?

Supply is price inelastic if a change in price causes a smaller percentage change in supply. (see the graph)👇

In that kind of situation any increase in demand expands Producer Surplus disproportionately (from Q1xP1 to Q2xP2).

What factors make supply price inelastic?

Operating close to full capacity

Supply is generally more inelastic in the short-term, because in the short-term capital is fixed. It takes time to invest and increase capacity

Limited factors of production - it makes a firm unable to increase supply (e.g. shortages of highly skilled labours).

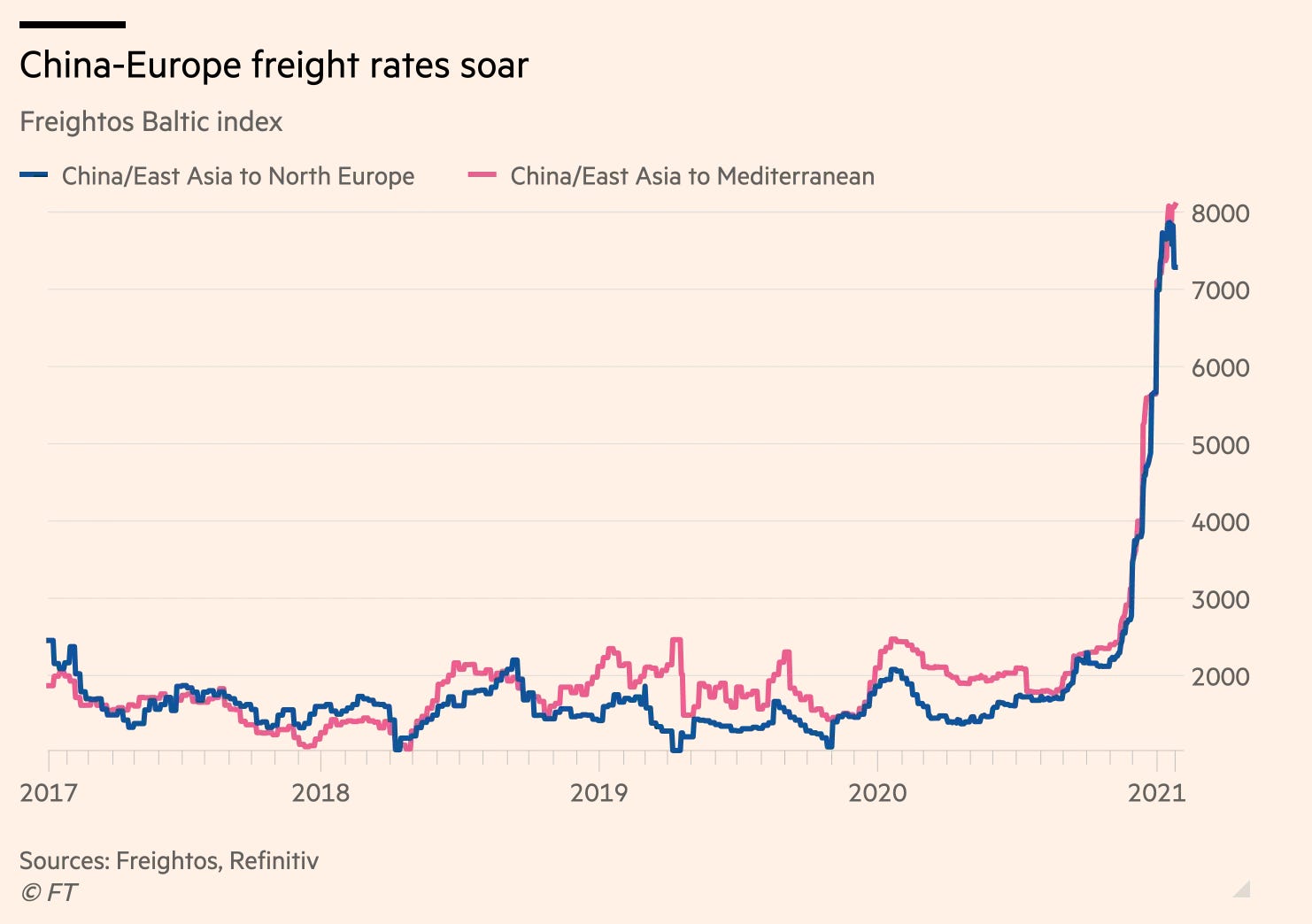

Here one of the examples of such situation -> shipping industry:

Cost to ship container from China to Europe grew 4-times(!) in the last couple of months due to strong demand and limited supply👇:

Not surprisingly, Maersk, the world’s largest shipping company announced last week that it expects to double its profit guidance vs. one from Feb’21.

Read FT article: Maersk doubles profit guidance for 2021 as Suez disruption pushes up prices or original A.P. Møller - Mærsk A/S guidance adjustment

(…) exceptional market situation now expected to continue well into the fourth quarter of 2021, the full year guidance for 2021 has been revised upwards with (…) an underlying EBIT expected in the range of 9-11bn (previously USD 4.3-6.3bn).

Where to look for those powerful suppliers?

There are plenty of such situations going on right now! Look at timber, steel, cooper or other commodities. It seems some cyclical companies might be able to deliver extraordinary results in next few quarters or even years.

I wish you a great returns for the rest of 2021 and beyond!

Thanks for reading!

Robert

————————————————————————————————

Disclaimer:

Robert Ditrych’s Newsletter is for informational purposes only and should not be relied upon as a basis for investment decisions. Clients of mine or myself may maintain positions in the securities discussed in this newsletter.

You should use the graph with demand & supply shift at the same time. Some of the supply is inaccessible due to bottlenecks (logistics).

As to cyclicals - watchout for too quick assessments. Outside of logistics nothing is assured rn, second- & and third-order effects could perturbate lots of businesses that seem to be beneficiary but in the end could be casualties.